03/16/2023

Shipments tick up, but ocean carriers positioned to capture potential trade gains

Air cargo is often moved on large pallets carried on the main deck of dedicated cargo jets. Ground staff at Dallas-Fort Worth International Airport move a pallet in position with a tug (Photo: Jim Allen)

The air cargo market in March is marginally less dire than in the preceding months. After a year-long decline, a modest recovery in Chinese factory output following the Lunar New Year holiday, an increase in manufacturing exports, and a marginal improvement in inflation are contributing to a semblance of seasonal stability for global demand and interest rates.

Nevertheless, the future remains uncertain, despite early indications of a second-half economic recovery amid difficult economic conditions. If import and export activities increase, it is more likely that container shipping lines will benefit than airlines. In addition, the reintroduction of capacity due to the reinstatement of international passenger services and weak demand are exerting pressure on fares.

The usual peak season did not occur last fall, but air cargo executives noted that demand took a significant hit in December. Volumes have gradually risen in recent weeks after a sluggish start to the year, as per analysts and data services. Market intelligence firm Xeneta reports a 2% week-over-week increase in volumes, with several air corridors between Asia, North America, and Europe experiencing heightened activity.

Xeneta's research last week showed a 4% year-over-year decline in demand for February, while the International Air Transport Association (IATA) reported a 14.9% drop in traffic for January. Shipment levels had been around negative 8% or lower compared to the previous year for several months, making February's figure an improvement. However, February comparisons may be distorted due to the Chinese New Year occurring earlier in 2023 than in 2022.

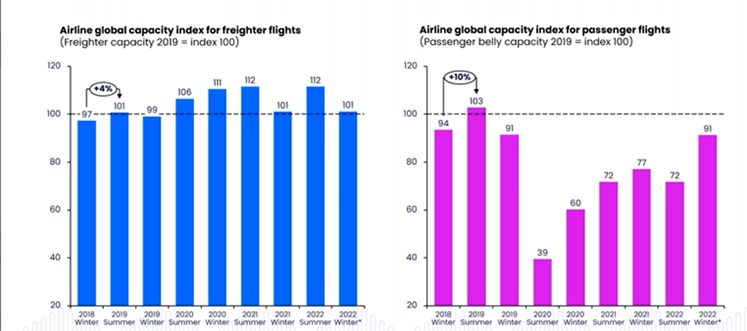

In February, total cargo capacity increased 11% for the second consecutive month, reaching pre-pandemic levels for the first time after a year of consistent growth. In response to the robust recovery in passenger travel, airlines are deploying more cargo-capable aircraft with larger lower holds. Since last summer, passenger belly capacity has increased by nearly 20 percentage points, while freighter capacity has decreased by over 10 percentage points, according to an analysis by Xeneta.

Aviation experts believe that cargo-only airlines are beginning to mothball older, less fuel-efficient aircraft that were profitable to operate during the height of the COVID-19 crisis, when freight rates soared. Beginning in April, more passenger aircraft are expected to enter the market during the busy summer season. The swift removal of all COVID travel restrictions in China and Hong Kong has unleashed pent-up demand for travel in Asia and prompted airlines to swiftly reintroduce grounded aircraft, which will increase transport supply on major trade routes.

This month, Teleport, AirAsia's air logistics arm, will resume 18 cargo routes to China using a combination of passenger airlift and chartered freighters from third parties. By July, the company hopes to have 40 routes from Malaysia, Thailand, and the Philippines.

According to Xeneta, soft demand has decreased load factors by eight percentage points compared to the end of 2022, with planes being only 57% full on average. This average may be deceiving, however, as passenger aircraft frequently operate routes with limited cargo capacity, whereas freighters typically fill more space.

Freighter and passenger belly capacity are going in opposite directions after the pandemic cool-down in freight (Source: Clive Data/Xeneta)

One way to assess capacity, in addition to weight, cubic space occupied, and weight multiplied by the distance carried, is aircraft utilization. In February, freighter flight hours experienced an estimated 4.7% reduction, showing improvement from January's 8.1% decline and December's 9% decrease, as reported by investment bank BMO. The three-month moving average of flight hours saw a 7.4% drop, marking the steepest decline in three years.

FedEx (NYSE: FDX) revealed an 81% fall in its Express segment's operating for the third quarter on Thursday, stating that it will further cut flight hours in the current quarter due to persistently low demand. Atlas Air, Air Transport Services Group, Cargojet, and Sun Country—all of which offer outsourced transport for Amazon Air and other large clients—have recently reported reduced aircraft utilization or anticipated activity declines this year. This is notable as it demonstrates that the air cargo downturn is spreading beyond general cargo to express shipments, which were sustained longer by the e-commerce boom. A Maersk Air Cargo spokesperson mentioned that demand for its new Asia-U.S. route was extremely soft at the beginning of the year.

In fact, according to Xeneta data, the air cargo market would have shrunk over the past four years if it weren't for express shipping, which has been fueled by the rapid growth of online shopping, and special cargo, such as pharmaceuticals. IATA reported that air cargo traffic decreased by 8% in 2022 compared to the previous year's record and decreased by 1.6% compared to pre-COVID levels. The organization forecasts that air cargo volumes will continue to decline this year, falling to levels 5.6% below those of 2019.

Semiconductors and consumer electronics serve as major indicators of air cargo demand. The World Semiconductor Trade Statistics Organization recently forecasted a 4.1% decrease in annual global chip sales for 2023. International Data Corp. revised its forecast for PC and tablet shipments, predicting 11.3% fewer units will be shipped in 2023 compared to 2022, as COVID restrictions have eased and commercial backorders for PCs are mostly fulfilled. Worldwide smartphone shipments are expected to fall by 1.1% this year, following an 11% decline last year due to inflation and weak consumer demand. In the fourth quarter, smartphone shipments dropped by 18.3%, marking the largest-ever decline in a single quarter.

Intra-Asia air cargo demand is higher than that from Asia to North America and Europe. Analysts attribute this to the recent diversification of supply chains beyond China, driven by the China Plus One strategy and the Regional Comprehensive Economic Partnership trade agreement that came into effect a year ago.

The Freightos Air Index, available through SONAR, shows how rates for exports from China to Europe have dropped 40% from a year ago, but are still 87% better than before the pandemic

These price reductions have resulted in decreased revenues and yields for carriers and logistics providers, despite the fact that businesses value lower shipping costs when moving goods. Spot rates, which fluctuate and vary by regional market, have decreased by about a third compared to this time last year but are still 55% higher than they were prior to the pandemic. Experts in air logistics anticipate that the new baseline will eventually settle slightly below the current level but still above the 2019 level.

As legacy contracts with higher rates expire, the negotiating leverage of carriers diminishes. As commitments for allocated space expire in March for eastbound trans-Pacific and eastern Asia-to-European traffic, new rates under negotiation will be typically 15% to 20% lower than the prior year but still higher than current market rates, according to a recent customer update from Taiwan-based logistics specialist Dimerco. Due to ongoing uncertainty, freight forwarders may be hesitant to sign long-term contracts with airlines.

Glass half full and half empty

Due to the global economic slowdown, high inflation, the Ukraine conflict, and rising jet fuel costs, the air cargo industry faces persistent challenges. In addition to impeding consumer spending in Europe, the Ukraine conflict has effectively reduced air cargo capacity by compelling airlines to circumvent restricted Russian airspace, resulting in several hours of additional detour time. Recent statements by Lufthansa Cargo executives indicate that longer routes between Europe and Asia have reduced the utilization of 1.5 aircraft, or approximately 11% of the company's fleet. The CEO, Dorothea von Boxberg, stated that increased passenger airlift may not have a significant impact on cargo demand this year due to the fact that the additional fuel carried will limit additional cargo capacity.

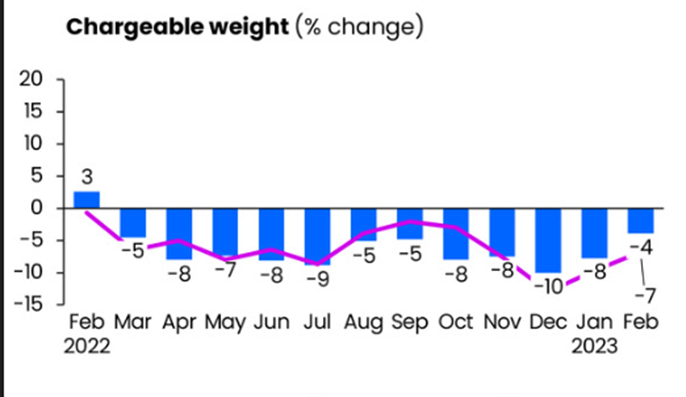

Air cargo growth has been negative since March 2022 (Source: Xeneta)

Despite numerous obstacles, such as the ongoing global economic slowdown, high inflation, the Ukraine war, and rising jet fuel costs, the air cargo market has experienced a slight improvement in recent months. Despite recent declines in oil prices, jet fuel remains 50 percent more expensive than it was four years ago, with these costs reflected in surcharges that significantly support airfreight rates. Additionally, airlines and airport cargo terminals face labor shortages, extreme weather, and union actions, which all increase costs.

Positively, there are indications of a trade recovery that could lead to an increase in air shipments. After an extended holiday break, Chinese factories have resumed production, with some shippers using air transport to make up for the downtime. Importers and exporters no longer need to be concerned about COVID-related factory shutdowns, as the Chinese government has modified its stringent eradication policies.

Air volumes and rates on outbound lanes from South China have strengthened in the past couple of weeks, particularly to North America, as per the latest data from price reporting agencies and logistics companies. Although the rates are about 45% lower than a year ago, they are still 80–90% higher than before the pandemic. New export orders are growing in several major economies and stabilizing in the US and China, according to the Purchasing Managers' Index. Inflation is also easing in G-7 countries.

Numerous logistics providers anticipate an increase in international orders and shipping activity in the second half as retailers clear out excess inventory and recommence placing new orders. However, airfreight may not benefit significantly from the increased trade, as the increased dependability of ocean freight and significantly lower rates make air transport less attractive.

The National Retail Federation forecasts that March import volumes at U.S. seaports will be 11% higher than in February and 8% higher than four years ago, with volumes rising steadily through at least July and exceeding 2019 levels. However, according to Niall van de Wouw, chief airfreight officer at Xeneta, many shippers may still opt for less expensive modes of transport, which could result in no growth for general air cargo by the end of the year. In a more pessimistic scenario, the demand for air cargo may not recover substantially until 2024.

MintN

Hot News

08/05/2024

Hot News

02/23/2023

Hot News

02/23/2023

Hot News

02/06/2023

Hot News

02/07/2023